Best Way to Convert SGD to USD: Banks vs Fintechs vs Stablecoin FX

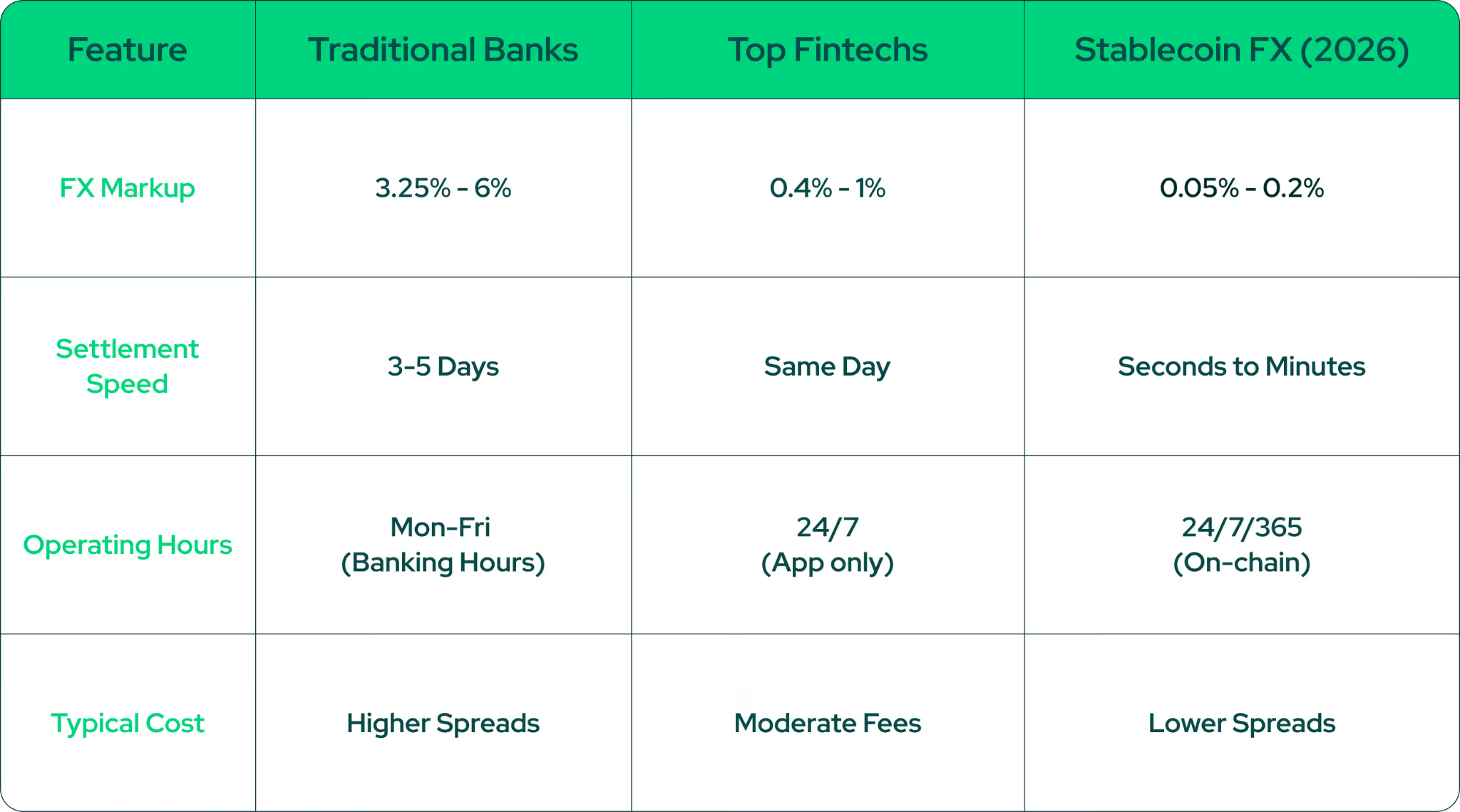

• Banks are trusted for SWIFT transfers, but remain the most expensive way to convert SGD to USD due to FX markups, correspondent fees, and multi-day delays.

• Apps like Wise, Revolut, and YouTrip are ideal for travel and retail, offering lower fees, upfront pricing, and faster same-day transfers but still rely on traditional banking rails for remittance providing.

• Stablecoins settle on-chain near real-time without correspondent bank layers, making them highly efficient for frequent cross-border transfers and institutional treasuries.

• Traditional T+2 settlement requires providers to bake a costly "risk buffer" into exchange rates. Stablecoins settle near real-time, eliminating this buffer to offer structurally tighter spreads.

• In line with the upcoming Singapore's MAS Single-Currency Stablecoin (SCS) framework and as a licensed Major Payment Institution (MPI), StraitsX maintains safeguards through 1:1 segregated reserve backing and regular independent audits.

For decades, moving money across borders was a "black box" of unpredictable fees and 3-to-5-day waiting periods. Fintechs such as Wise, Revolut, and YouTrip improved that experience by offering faster transfers and clearer exchange rates.

As we move through 2026, a new alternative has matured into an institutional-grade rail: Stablecoin-powered FX. For anyone who moves money regularly, whether you're sending funds overseas or are just tired of checking what the "real" rate actually is, it is worth understanding how it works and where it fits alongside the options you already use.

Why are Traditional Banks Expensive for SGD to USD Transfers?

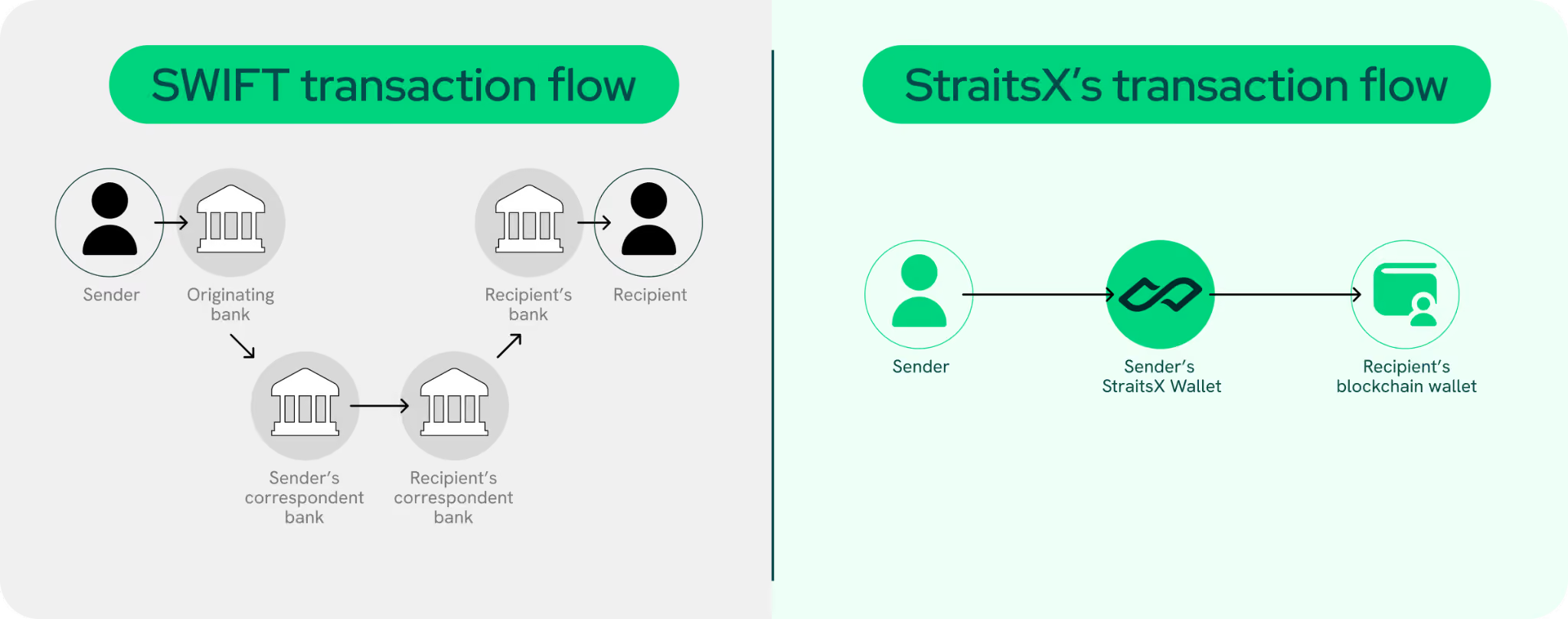

Banks have always been the default for international transfers using the SWIFT network, and for good reason. Banks are widely accepted, and handle everything from wire transfers to bank drafts. While this system is globally trusted, it often comes with trade-offs:

- Transfers can take 2–5 business days

- Exchange rates may include spreads and intermediation costs

- Payments are limited to banking hours

In contrast, stablecoins reduce the layers involved in correspondent banking, which can introduce additional spreads, liquidity buffers and settlement delays. Recent industry reports on cross-border friction highlight how stablecoins are replacing these fragmented correspondent banking chains with blockchain-based settlement networks, bypassing the need for expensive pre-funding.

- The Bank Way: Sender → Bank A → Correspondent Bank B → Correspondent Bank C → Recipient Bank.

- The Stablecoin Way: Sender Wallet → Blockchain → Recipient Wallet.

How Fintech Modernizes the “Money Moving” Experience

Fintech companies like Wise, Revolut, and YouTrip were the pioneers that first challenged the banking status quo. By prioritizing pricing transparency and streamlining the user interface, these platforms achieve speed and lower costs by maintaining local liquidity pools in various countries.

Instead of sending money across borders via SWIFT, they "net" transfers internally, meaning when you send money, the platform often just moves funds between its own local bank accounts in the origin and destination countries. This is a significant advantage for frequent or aggregated transfers, as it provides a more predictable internal settlement process that reduces reliance on cross-border SWIFT messaging.

However, most fintech services still operate as Remittance providers built on top of traditional banking rails. On the backend, fintechs rely on regional payment systems and bank processing windows, which means they are not "instant" in terms of settlement finality. Since they effectively aggregate traditional liquidity, fintechs must still account for the bank settlement delays, often resulting in rates that, while good, still carry an aggregator's markup.

Why Settlement Speed Affects the Rates Offered

When you convert currency through a traditional bank, the transaction doesn't actually finalise for 2–3 business days after you initiate it. This is known as the T+2 settlement. During that window, exchange rates can move, and to protect against that risk, banks build a buffer into the rate they quote you. This pricing reflects the role banks play in providing guaranteed settlement and managing market and credit risk across the settlement cycle.

Stablecoin transactions on the other hand, are settled in minutes, directly on-chain. There's no waiting window, which means there's no buffer needed. The rate you're quoted reflects closer to the actual market rate at that moment.

Research from the BIS Project Mariana has shown that near-instant settlement removes the credit risk window that traditional FX pricing has to account for allowing for tighter rates as a direct result. It's a subtle difference, but it's one reason why stablecoin FX spreads tend to be structurally tighter, because the risk that traditionally gets priced into the rate simply doesn't exist in the same way.

The Difference Behind the Numbers

When a bank or traditional FX provider quotes you a rate, that rate includes their margin baked in. The spread, the difference between the buy and sell price, is a core component of FX pricing and revenue models

Fintech apps narrowed that spread significantly by being more efficient and transparent about their fees. But their rates are still ultimately sourced from the same underlying forex markets, which means some of that inherited cost remains.

Depending on the platform and the size of your transfer, a Stablecoin FX conversion might be filled through an exchange order book, an OTC desk, a market maker, or an on-chain liquidity pool, often a combination. Because these channels operate around the clock and don't carry the same overhead as traditional banking infrastructure, the resulting spreads tend to be tighter.

That said, the rate you get still depends on a few things, mainly how much liquidity is available for your currency pair at that moment. For common pairs like XSGD/XUSD, liquidity is generally deep enough that the rates are competitive. However, for larger transfers or less common pairs, it's always worth checking the actual rate before committing.

¹ DBS Overseas Fee Guide & World Bank RPW Database ² Revolut vs. Wise vs. Youtrip Comparison (2026) ³ Uniswap v3 Protocol Tiers & BIS Project Mariana Report

Why Regulatory Compliance Matters

As stablecoin adoption grows, regulatory frameworks are emerging to ensure transparency and reserve backing. In Singapore, stablecoins are set to be governed by the Monetary Authority of Singapore (MAS)’s upcoming Single-Currency Stablecoin (SCS) Framework, while conversion between stablecoins and fiat currencies typically falls under Singapore’s existing Payment Services Act (PSA) framework

As a Major Payment Institution (MPI) licensed by the MAS, this means the rails we provide, and the assets we use, such as XSGD and XUSD, are designed to be compliant with strict institutional standards:

- 1:1 Reserve Backing: Every token is backed by high-quality liquid assets held in segregated accounts.

- Regulatory Recognition: Assets like XSGD and XUSD (issued by StraitsX) are recognized as substantively compliant with the upcoming SCS framework.

- Bank-Grade Audits: Monthly independent attestations and annual audits ensure that reserves are always present and accounted for.

Conclusion

In 2026, traditional FX rails continue to serve many use cases, though newer alternatives offer improvements in speed and cost efficiency. Organisations using traditional FX infrastructure may have opportunities to enhance settlement times and reduce costs.

The "best" way to swap SGD to USD depends on your specific operational needs:

- Use Traditional Banks for: Traditional branch support, physical bank drafts, or when a counterparty strictly requires a SWIFT-only transaction for internal compliance.

- Use Fintech Apps (e.g., Wise, YouTrip, Revolut) for: Daily consumer travel, retail spending at foreign merchants, and remitting everyday cross-border transfers where convenience and predictable pricing matter more than settlement mechanics.

- Use Stablecoin FX for: Institutional treasury and maximum margin efficiency, ideal for users and institutions already operating with digital asset infrastructure, prioritizing immediate capital finality via direct swaps over delayed remittance.

Moreover, transitioning to stablecoin liquidity doesn't require an overhaul of your entire financial stack. Our team specializes in helping clients across both traditional and digital finance systems integrate high-speed FX rails into their existing workflows, improving margins and achieving near-instant settlement.

Ready to see how the rates actually compare?

- Use our Live Swap Calculator: Input your amount and see real-time SGD to USD conversion now. No hidden fees, no "buffered" spreads, just the raw rate.

- Run a Comparative Cost Analysis: Speak to our Sales Team to see how much you can save by bypassing "T+2" settlement cycles and reducing correspondent banking fees.

- Review Regulatory Compliance: Understand how our infrastructure, designed to meet the rigorous reserve and transparency standards of the EU’s MiCA framework and U.S. stablecoin regulatory proposals such as theGENIUS Act, can protect your balance sheet.

- Test the Integration: Use our sandbox to simulate transactions and validate your setup before going live.

{{swapCal}}

Sources:

- https://www.mckinsey.com/industries/financial-services/our-insights/banking-matters/how-banks-can-win-back-lower-value-cross-border-payments-business

- https://www.mckinsey.com/industries/financial-services/our-insights/global-payments-report

- https://www.dbs.com.sg/personal/support/card-charges-and-fees-overseas-transaction-fees.html

- https://remittanceprices.worldbank.org/

- https://wise.com/sg/blog/revolut-vs-youtrip

- https://docs.uniswap.org/concepts/protocol/fees

- https://www.bis.org/publ/othp75.pdf

- https://www.mas.gov.sg/news/media-releases/2023/mas-finalises-stablecoin-regulatory-framework

- https://www.mas.gov.sg/regulation/payments/licensing-for-payment-service-providers

.avif)

.avif)